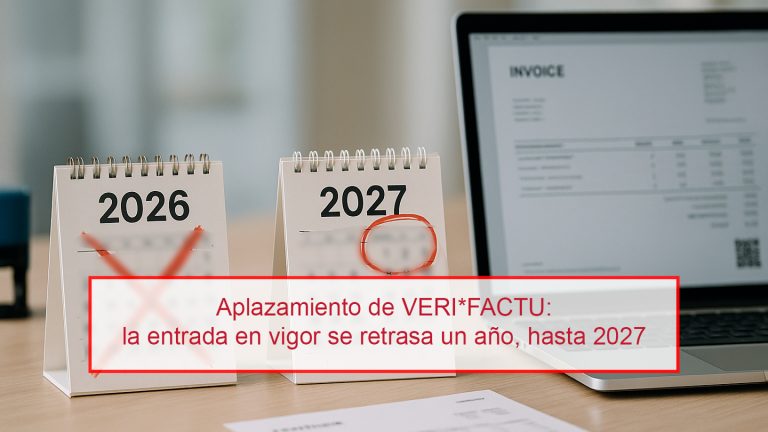

VERI*FACTU Postponement: Entry into Force Delayed by One Year, until 2027

On December the 2nd, 2025, the Council of Ministers approved Royal Decree-Law 15/2025, which postpones for one year the entry into force of the Obligations derived from the so-called VERI*FACTU Regulation (Verifiable Invoice Issuance System) and the requirements of the Computer Billing Systems regulated in Royal Decree 1007/2023.

This Royal Decree-Law must be validated by the Congress of Deputies within a maximum period of 30 days to remain in force, so, as of today, the postponement is approved but pending Parliamentary confirmation.

New VERI*FACTU Implementation Schedule

Until now, the planned entry into force schedule was as follows:

January the 1st, 2026: Companies subject to Corporation Tax.

July the 1st, 2026: other Companies and Self-Employed who use Computerized Invoicing Systems.

With the approved modification, the New Calendar is Now:

January the 1st, 2027: Companies that pay Corporate Income Tax.

July the 1st, 2027: other Companies and Self-Employed individuals required to use Computerized Invoicing Systems.

In other words, an additional year’s extension is granted for the technical adaptation to VERI*FACTU and the rest of the requirements of the Regulation of Computer Billing Systems.

What Does the New Regulation Say?

The fourth final provision of the Royal Decree-Law establishes that the Regulation and the Royal Decree itself will come into force the day after its publication in the Official State Gazette, but sets new deadlines for the adaptation of the Invoicing Systems:

The taxpayers referred to in Article 3.1.a) must have their computer systems adapted to the characteristics and requirements established in this regulation and its implementing regulations before the 1st of January 2027. The rest of the taxpayers mentioned in Article 3.1 must have the aforementioned computer systems operational before the 1st of July 2027.

What Hasn’t Changed

Although the enforceability is delayed, the Obligations do not disappear. Specifically:

The Obligation to adapt to VERI*FACTU and the Billing System requirements remains: Its entry into force is only postponed for 12 months.

The Objective of the standard remains the same: to guarantee the integrity, traceability and immutability of billing records and to fight against “dual-use” software and tax fraud.

Therefore, this is not a reversal, but an Extension of Deadlines.

How Does this Postponement Affect you?

In practice, this change means the following for your Company or Professional Activity:

More Time to Adjust You have an additional year to adapt your current Billing Software or hire a provider that complies with the VERI*FACTU Regulation.

The Investments made Remain Valid If you’ve already started making changes to your Billing System, those efforts won’t be lost. Adaptation will still be necessary; it’s just that the deadlines for having everything operational have been extended to 2027.

The Digitization of Invoicing Continues The Spanish Tax Agency is maintaining its roadmap towards a more digital, traceable, and controlled Invoicing System. Therefore, it is advisable not to half adapt projects and to continue planning them well in advance.

Programs already Purchased Remain Useful If you have already contracted an Invoicing Software adapted or in the process of being adapted to VERI*FACTU, you can continue using it normally and move forward with the configuration, as it will be mandatory in year 2027.

Recommendations for Companies and the Self-Employed

Even if the schedule is delayed, it is advisable to:

Review the Status of your Invoicing System and detect if it will need to be updated or replaced.

Contact your Software Provider to confirm the VERI*FACTU adaptation plan and the planned deadlines.

Plan the Implementation with a Buffer to avoid last-minute rushes in 2027.

Stay Informed Regarding the ratification of Royal Decree-Law 15/2025 in Congress and possible regulatory developments.

Javier has a degree in “Dirección y Administración de Empresas” (Business Management and Administration) from University of Malaga, he specialized in accounting and tax advice working in an office of recognized prestige for more than 16 years, joining Ruiz Ballesteros in December 2017 after the merger by absorption of Carrillo Asesores by Ruiz Ballesteros. He has developed his career as an internal consultant for companies and since 2003 as an external consultant, performing tasks of accounting, taxation and commercial law of companies from very diverse sectors. It has also been responsible for accounting a taxation of individuals, making quarterly fiscal statements of self-employed, as well as income statements, both residents and non-residents. His training is continuous through the development of different specialization courses. He speaks English and currently performs accounting and tax control tasks for groups of client companies.