Español

Español Русский

Русский

In difficult economic times, restructuring operations are a common way to achieve economies of scale, centralize and reduce costs, and generally improve the management of corporate groups.

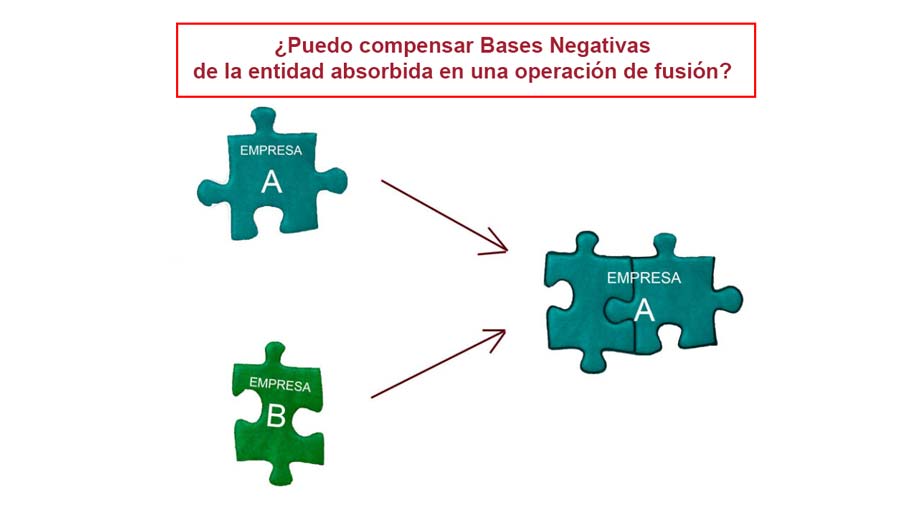

Merger transactions are often a common way to achieve these goals, but the question often arises as to what happens to the losses of the acquired entity: if it had outstanding tax losses, can the acquiring entity offset them?

Right to offset negative tax bases of the absorbed entity.

Chapter VII of Title VII of Law 27/2014, of November 27, on Corporate Income Tax, regulates the special tax regime applicable to restructuring operations.

Based on this regime, when the restructuring operation determines an universal succession, as occurs in the merger operation, and, therefore, the acquiring entity (absorbing) succeeds in the rights and obligations of the transmitting entity (absorbed), article 84.2 of the aforementioned tax neutrality regime establishes that “the negative tax bases pending compensation in the transmitting entity will be transferred to the acquiring entity”, and this provided that (i) the extinction of the transmitting entity occurs or (ii) the transfer of a branch of activity whose results have generated negative tax bases pending compensation in the transmitting entity.

In the latter case, only the negative tax bases pending compensation generated by the transferred branch of activity would be transferred.

Therefore, in principle, provided the transaction falls under the special tax regime, the acquiring entity could offset any outstanding tax losses arising from the acquired entity.

Limitation of the right when the entities involved in the merger are part of a business group.

However, when the entities involved in the merger are part of the same group of companies, pursuant to Article 42 of the Commercial Code, the amount to be offset would be reduced by the positive difference between the value of the partners’ contributions, made for any purpose, corresponding to their stake in the transferring entity, and its tax value.

We can see this with a numerical example:

Limitation in case of acquired shares.

The question arises as to what happens if the acquired entity, which carries negative tax bases, was previously acquired from a third party.

The limitation of the previous section also applies in this case, and the value of the contributions made by partners for any reason and, on the other hand, their tax value must be determined.

In this regard, the National Court ruled in its judgment 5158/2019 of December 12, 2019, where it resorted to a finalist interpretation of the rule and concluded that to calculate said limitation, the contributions made by the partners since the constitution of the participation must be used (as opposed to the literal interpretation that refers to the contributions made since the acquisition of the participation).

The Tax Inspectorate considered at the time that the tax losses incurred before the purchase of the portfolio by B could not be used by A.

The National Court ratifies this criterion by interpreting that the purpose of the rule is to avoid double exploitation of the same losses that could have arisen (and materialized, if applicable) in any previous partner (for example, by integrating the negative income from the sale of the shares or by tax-impairing the portfolio when either of these two losses were deductible).

Specifically, the National Court concludes that:

“When the transferring entity’s losses were incurred before the acquisition of the stake, the former partner will have deducted these losses for tax purposes, either by making the appropriate provision for depreciation of the securities portfolio or as a loss generated at the time of the transfer of the stake. However, if, after the merger, the profits obtained by the company resulting from said process are allowed to be offset against the transferring company’s outstanding BINs, the transferring company’s losses would be used twice, which is precisely what Article 90.3 of the TRLIS seeks to prevent.”(Current article 84.2 of law 27/2014).

And, he refers to a Supreme Court ruling of December 13, 2012 (rec. 251/2010), which concluded that:

“although, indeed, it is possible that the previous partners who bore the loss were not able to effectively apply it in their relations with the Spanish Treasury, this circumstance may arise not only when they are non-residents in Spain but also in cases where they are residents (consider the case where the allocation to the provision for depreciation of securities had generated a negative tax base for the former partner that could not be offset due to the expiration of the deadline for doing so), however, the LIS does not require, in order to apply the limitation to the offsetting of the negative tax bases of the transferring company by the acquiring company, that the tax loss of the former partners has been effectively applied by them, limiting itself to stating objectively that in the event that the acquiring entity participates in the capital of the transferring entity, the negative tax base susceptible of offset will be reduced by the amount of the positive difference between the value of the contributions of the partners corresponding to said participation and its book value, without requiring that the losses borne by the former partners should have been, in order to apply the limitation, effectively applied in Spain”.

To clarify this matter, we attach the example of the specific numerical case that was raised in the analyzed Sentence, which was the following:

Existence of a valid economic reason.

Without prejudice to the foregoing, it is important to remember that in order to apply the special regime that allows the use of the negative tax bases of the absorbed entity, there must be a valid economic reason to justify the restructuring operation.

Article 89.2 of the Corporate Income Tax Law stipulates that the special regime is not applicable “when the transaction carried out has as its main objective fraud or tax evasion”, this circumstance occurring when “the transaction is not carried out for valid economic reasons, such as the restructuring or rationalization of the activities of the entities participating in the transaction, but for the sole purpose of obtaining a tax advantage.”

It is therefore vitally important that before carrying out a restructuring transaction, the parties involved obtain appropriate advice to avoid tax risks arising from the incorrect application of the special tax neutrality regime or, in general, any other tax incentive or benefit.