Español

Español Русский

Русский

Sometimes the Tax Agency carries out inspections because it suspects that some legal figure is being used with the sole intention of reducing taxation, in which case it usually resorts to article 16 of Law 58/2003, of December 17, General Tax Law (hereinafter, LGT), to justify the “simulation” of a legal transaction and apply a […]

mercantile law

18

Dec

Dec

Do you work on commission? If so, you should know that the legal status of a commission agent is often confused with that of a sales agent, as they share some similarities. We’ll explain the main differences between these two concepts, according to current legislation, so you can determine which contract is best for you. […]

05

Sep

Sep

The valuation of shares or participations company’s valuation is a requirement for tax purposes due to various circumstances that may arise in the lives of citizens and businesses. Correctly determining the value from a tax perspective depends on the circumstances that require the valuation, such as the sale of shares, a donation, an inheritance, a […]

04

Sep

Sep

As corporate restructuring transactions, securities exchange transactions are eligible for the special tax regime for mergers, spin-offs, asset transfers, and securities exchanges, which we have discussed in previous articles. Specifically, Article 76.5 of the Corporate Income Tax Law defines them as: “An exchange of securities representing share capital shall be considered to be an operation […]

04

Sep

Sep

This article is a continuation of the article “The merger of companies. General aspects” and aims to analyze one of the so-called “Special Mergers” regulated in Section 8 of Title II of Law 3/2009 on structural modifications (LME). This type of merger is characterized by the fact that the law provides for the possibility of […]

04

Sep

Sep

The purpose of this article is to analyze one of the so-called “Special Mergers” regulated in Section 8 of Title II of Law 3/2009, on structural modifications (LME), specifically those regulated in article 49.2 LME, in which the acquiring company absorbs a wholly-owned subsidiary indirectly, in this way the company would absorb a subsidiary of […]

04

Sep

Sep

This article is a continuation of the article “The merger of companies. General aspects” and aims to analyze one of the so-called “Special Mergers” regulated in Section 8 of Title II of Law 3/2009, on structural modifications (LME), specifically the so-called reverse mergers, in which the absorbed company directly or indirectly owns the shares or […]

04

Sep

Sep

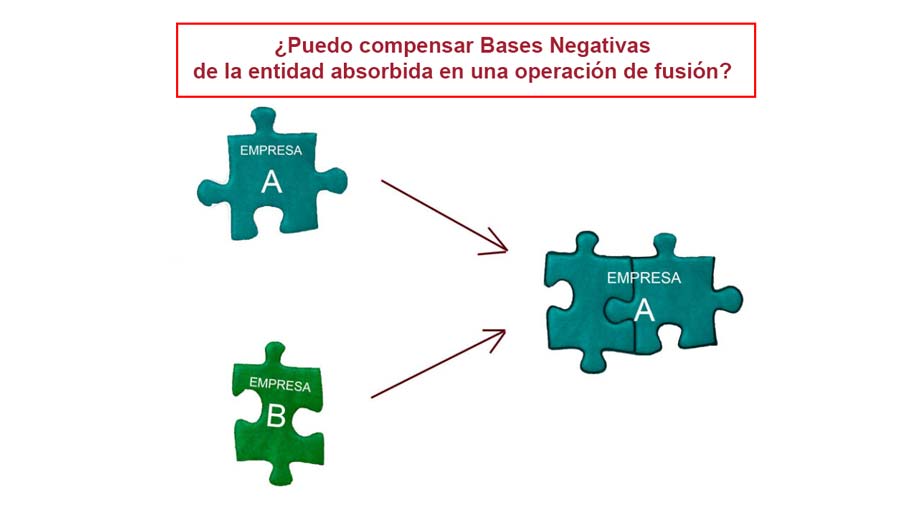

In difficult economic times, restructuring operations are a common way to achieve economies of scale, centralize and reduce costs, and generally improve the management of corporate groups. Merger transactions are often a common way to achieve these goals, but the question often arises as to what happens to the losses of the acquired entity: if […]

04

Sep

Sep

Corporate divisions, commercial and tax aspects The corporate division restructure operation must be addressed from both a commercial and tax perspective, since the different types of divisions are regulated not only by the Structural Modifications Law (hereinafter, LME) but also by the Corporate Income Tax Law (hereinafter, LIS). It is important to review both regulatory […]

02

Aug

Aug

Competence of the General Meeting or does it depend? Article 160 of the Capital Companies Law (hereinafter, LSC) includes those matters whose resolutions must be approved by the general meeting, and which are excluded from the powers of the company’s administrative body. Competence of the General Meeting. Social object of the company. In accordance with […]