Español

Español Русский

Русский

Sometimes the Tax Agency carries out inspections because it suspects that some legal figure is being used with the sole intention of reducing taxation, in which case it usually resorts to article 16 of Law 58/2003, of December 17, General Tax Law (hereinafter, LGT), to justify the “simulation” of a legal transaction and apply a […]

Tax law

17

Dec

Dec

On July the 9th, 2021, Law 11/2021, on measures for the prevention and fight against Tax Fraud, was published. This law has brought about significant Tax changes. In this article, we will focus on one of them, which corrects the surcharges applied when Tax Returns are filed late. Specifically we are referring to section 2 […]

03

Dec

Dec

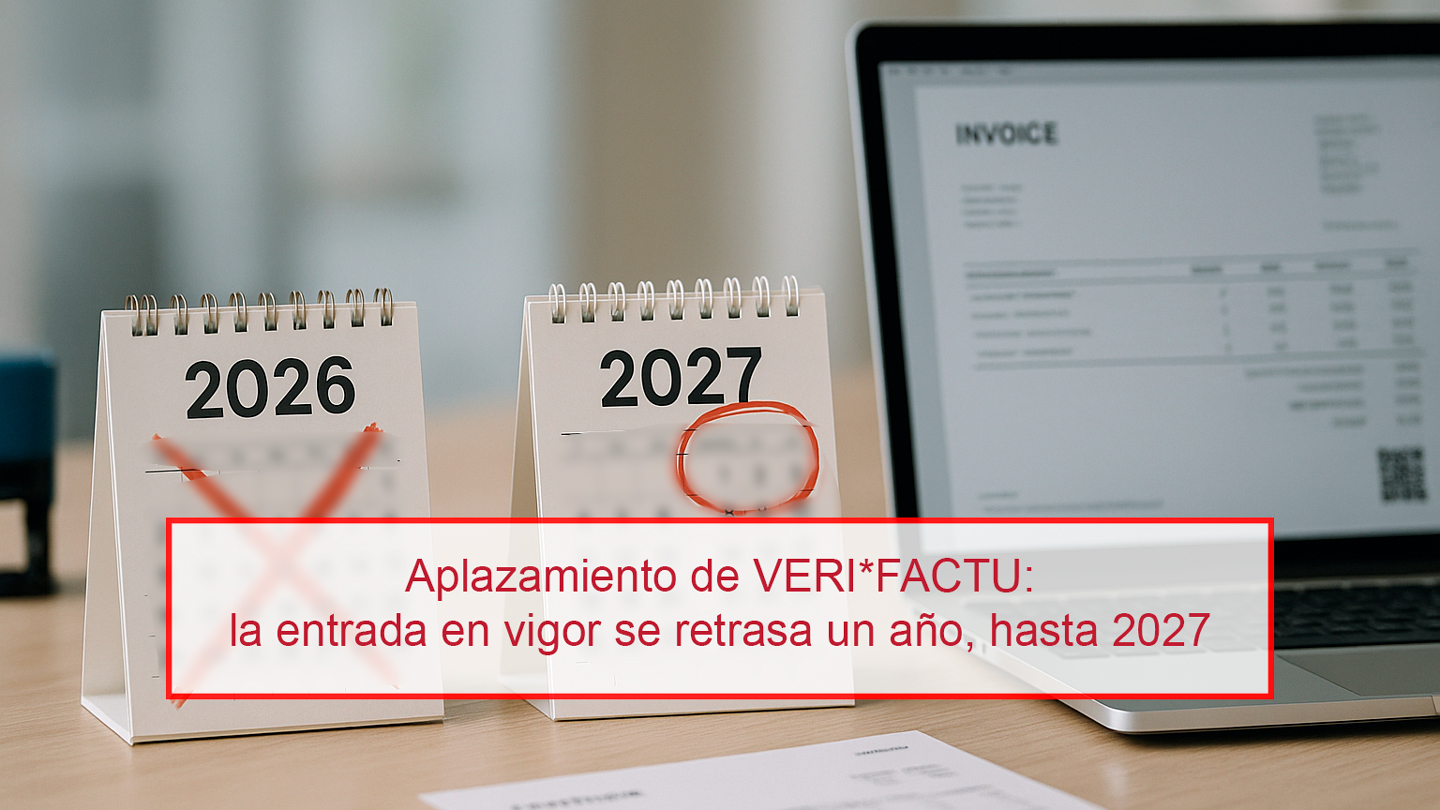

On December the 2nd, 2025, the Council of Ministers approved Royal Decree-Law 15/2025, which postpones for one year the entry into force of the Obligations derived from the so-called VERI*FACTU Regulation (Verifiable Invoice Issuance System) and the requirements of the Computer Billing Systems regulated in Royal Decree 1007/2023. This Royal Decree-Law must be validated by […]

05

Sep

Sep

The valuation of shares or participations company’s valuation is a requirement for tax purposes due to various circumstances that may arise in the lives of citizens and businesses. Correctly determining the value from a tax perspective depends on the circumstances that require the valuation, such as the sale of shares, a donation, an inheritance, a […]

05

Sep

Sep

Personal income tax is a direct, personal tax levied on the income of individuals, based on their personal and family circumstances. There are several exempt incomes, detailed primarily in Article 7 of Law 35/2006, of November 28, on Personal Income Tax (hereinafter, IRPF). We will specifically refer to those included in section “p” of the […]

04

Sep

Sep

As corporate restructuring transactions, securities exchange transactions are eligible for the special tax regime for mergers, spin-offs, asset transfers, and securities exchanges, which we have discussed in previous articles. Specifically, Article 76.5 of the Corporate Income Tax Law defines them as: “An exchange of securities representing share capital shall be considered to be an operation […]

04

Sep

Sep

When selling a property, whether it’s the result of an inheritance or a divorce decree, it’s common to wonder about its value and the date of acquisition. This is an important aspect because it directly impacts the calculation of the capital gain upon sale. WHAT IS MEANT BY CAPITAL GAIN? Article 33 of Law 35/2006, […]

04

Sep

Sep

On December 30, 2020, Law 11/2020, the General State Budget (LPGE), was approved. The LPGE is usually approved every year, however, curiously, we had gone two years without a new Budget Law, as the political community had been unable to agree on new budgets. With the General State Budget Law they are now approving, they […]

04

Sep

Sep

As a continuation of the previous article (I want to donate a property to my child: I. What should I bear in mind?), we proceed to analyse this same donation case in the event that the donors did not have only one descendant. But what if I want to donate the property to one of […]

05

May

May

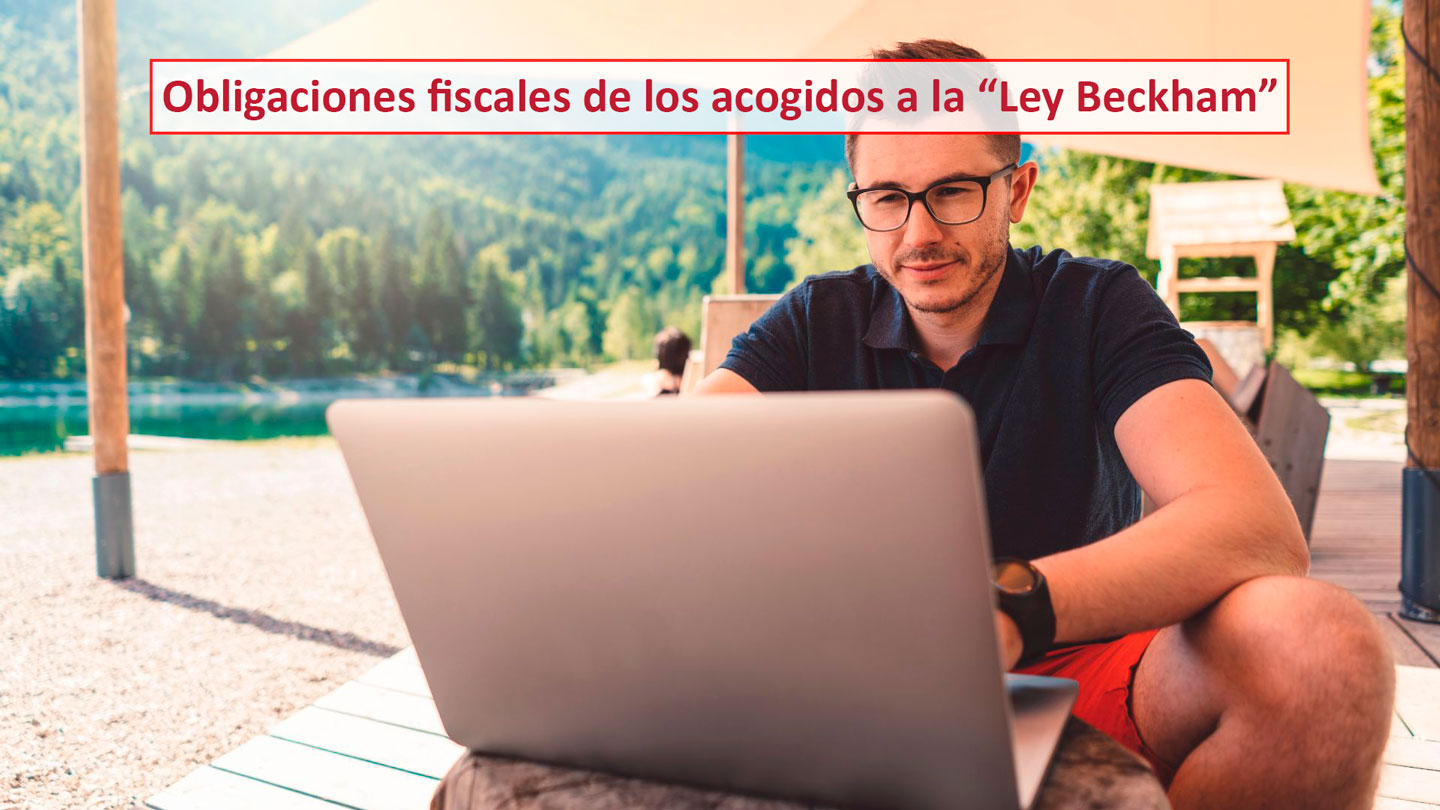

The Special Regime for workers, professionals, entrepreneurs, and investors who relocate to Spanish territory, also known as the “Beckham Law,” is regulated under Article 93 of Law 35/2006, of November 28, on Personal Income Tax (hereinafter, LIRPF). This special regime allows certain taxpayers who move to Spain to be taxed as non-residents, which may be […]