Español

Español Русский

РусскийToday we are discussing a very special case that we are sure you’ll find interesting. Suppose that we establish a company to construct one single house, and while we are building it a buyer appears who wants to take over the company, that is to say, they will be directly acquiring the company shares and […]

Author Archives: Jesús R. Ballesteros

02

Jun

Jun

The true taxation of the costs of judicial procedures is difficult to answer. We must first focus on the question and the concept of costs, since they are considered a credit to the prevailing party. However, this credit is different from the credit that comes from a service leasing contract between the lawyer and the […]

02

Jun

Jun

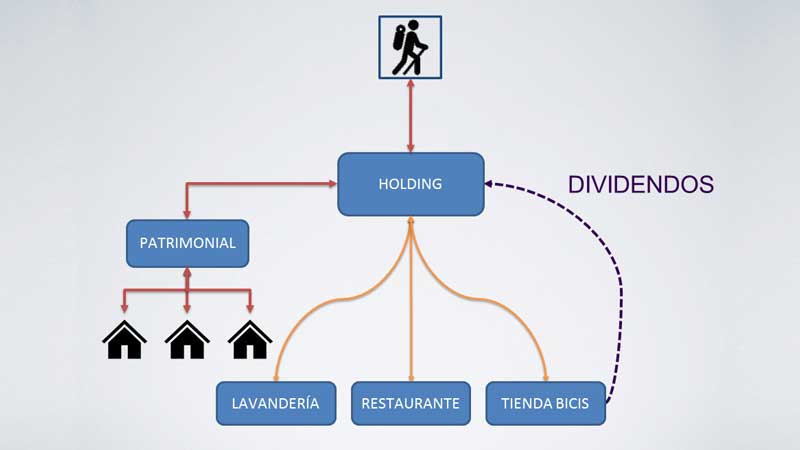

Exemption from Corporate Taxation This is a little more “special” than our usual articles, because we are going to attempt to explain one of the corporate restructuring operations which is considered “complex”, but which, if executed well, can save us a significant amount of tax and allow us to re-organise our corporate and personal assets. […]

12

May

May

or “The Art of Investing and Not Paying for Profits” In January 2015, Article 21 of the Spanish Corporate Tax Law (hereafter LIS) changed significantly, a modification which is not very well known at this time, but is key to investing in Spain and not paying tax for selling another company’s shares. We are referring […]

12

May

May

We are currently experiencing a boom in the rental of so-called “holiday apartments”, caused by the increase in tourists and the tourist sector in general that Spain is suffering. There are many doubts surrounding the taxation of this type of rental, so, in this post, with the help of our tax lawyers, we’re going to […]

18

Mar

Mar

[toc] 1. PURPOSE OF THE DOCUMENT We issue a new extraordinary note to inform all our clients firsthand about the measures that the Government of Spain has taken to palliate the coronavirus crisis, published on 18 March 2020. These measures attend to business, labor, tax and personal aspects of all Spanish people. Support measures for […]

22

Feb

Feb

New developments in taxation for 2017 As from 1st January 2017 it is illegal to pay more than 1,000 euros in cash. On 2nd December 2016 the Spanish Cabinet passed a Decree-Law which reduces the amount of cash payments to 1,000 euros (up until now the limit was 2,500€), as payment for any goods or […]

01

Dec

Dec

People considered Non-Resident for Tax Purposes in Spain have two ways of obtaining some kind of revenue (income): either through a permanent establishment or without any permanent establishment being involved. In the first case, with a permanent establishment[1], tax is paid on the entire revenue attributable to that establishment, regardless of the place where the […]

29

Nov

Nov

Continuing on from our previous article, let´s assume that we are a company, that first we bought a plot of development land and on this land we have built ten apartments, we have paid VAT on the purchase of the land and also during the construction of the apartments, as we have contracted the services […]

28

Nov

Nov

If you have read our previous post “When do we apply VAT to a purchase of urbanised land“, you will know that we are buying a plot of land that is urbanised or in the process of being urbanised, for which we will be paying VAT at 21 %. Assuming for example that the price […]