Español

Español Русский

Русский

In a company, the decision to finance the purchase of a property with a financial product or other is not insignificant.

In the majority of cases a mortgage is used, however, there are other finance products that deserve to be studied, particularly property leasing, in order to make an educated decision on how to acquire an industrial warehouse or commercial premises.

What is a property lease?

A lease is a financial rental, a contract through which a company can use a property, whether moveable or immoveable, in exchange for some regular payments. It is a necessary requirement that said contract includes the possibility that the option to purchase the property used can be exercised upon its termination.

Requirements that must be included in said contract from a tax perspective:

Article 106 of the Spanish Corporate Tax Law 27/2014, of 27th November, establishes that:

- The lesser must be a credit company or a financial establishment.

- The tenant must use the property leased to carry out its economic activity.

- The minimum duration of the contract will be two years for moveable property and ten years for immovable property.

- The payment must be stated in the contract, distinguishing between the recovery part of the cost of the transferred property and the financial burden part.

- The contract must include the option to purchase.

Advantages of a property lease, with regards to the mortgage loan:

- In the lease, the total value of the property can be financed. For a mortgage, it is normal that the purchasing company must pay 40% or even 50% of the price plus expenses, while for a lease they can finance up to 100%.

- The financial charge paid by the leasing entity is considered to be a tax-deductible On the other hand, in the mortgage the expense will always be the depreciation only, which will usually be between 2% and 3% of the property’s price per year (excluding the grounds), meaning that it takes between 33 and 50 years to provide us with the full expense.

- The VAT applicable to the lease is paid with each payment when it is made, in such a way that no single significant disbursement is necessary and the VAT paid each month/semester compensates us.

- The part of the property corresponding to the construction value can be depreciated in an accelerated manner. Said tax depreciation will never exceed the sum of adding the double of the linear depreciation coefficient to the property’s cost according to the officially approved depreciation tables for said property. For smaller companies, the double of the linear depreciation coefficient will be taken according to the officially approved depreciation tables and will be multiplied by 1.5, which in practice will result in a depreciation three times greater than usual (1.5 x 2 =3) on the accounts. This generates a difference between the accounts and the tax depreciation, that is, we are deferring (delaying) the corporate tax payment.

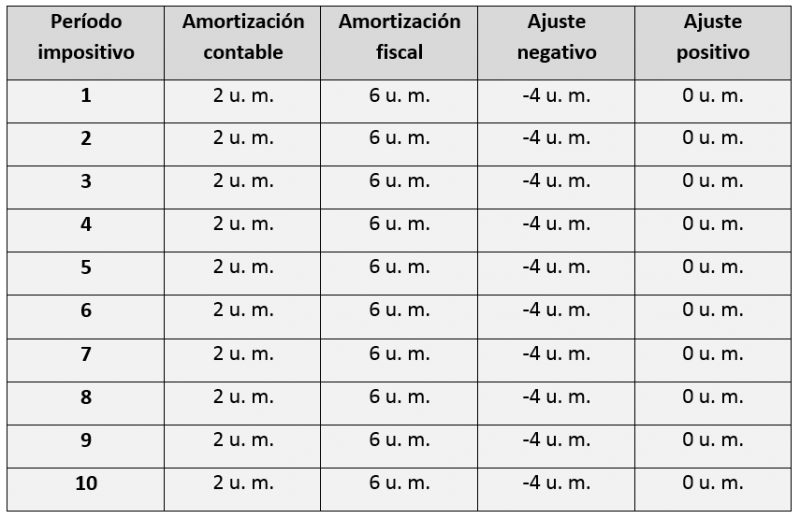

Example of the Acquisition of a Property through a Lease:

- A formalised lease for the acquisition of an office by a smaller company, with a duration of 10 years and a property costing 100 currency units (100 E.C.U.).

- According to the tables, the depreciation coefficient is 2% (50 years).

- It is certain that the option to purchase will be exercised.

Positive and/or negative adjustment that would have to be carried out for the payment of the Corporate Tax would be:

From tax period number 16 we would have:

What at first is a relief in the treasury becomes the opposite when it is reversed. This must be thoroughly assessed, especially taking care of the financial expense of each company, hence the importance of financial and tax analysis before acquiring any properties. In other words, we have depreciated the property in just over 16 years, therefore, until period 17 a negative adjustment is made to the accounting profit, so that the taxable income of the corporate tax is reduced by the amount of this adjustment. In that case, from period 18 to 50, this is reversed by having to make a positive adjustment in each period, which is when we start paying the deferred tax.

If you found this article interesting, please feel free to share.